Spicejet: High Risk, High Drama and a Possible Turnaround?

August 21, 2025

Once India’s second-largest domestic carrier with >20% market share, SpiceJet now stands at a critical juncture — burdened by litigations, debt, and an aging fleet, yet surviving through timely fundraises and management resilience. With market share now below 3%, it is viewed as a high-risk turnaround bet — where the challenges are glaring, but potential catalysts such as fleet re-induction, cargo strength, and operating leverage continue to keep investor interest alive.

Why one should not touch it – Risks in abundance:

- Low fleet size resulting in inefficiencies: After a long period of losses, Spicejet might just be breaking even wrt to operations, but to achieve numbers with limited fleet, they are running with extremely tight schedules resulting in multiple flight delays, cancellations, stress on the staff etc.,

- Aged fleet: Spicejet’s fleet is the oldest amongst its peer with an avg age of >14 years, which results in higher maintenance and lower customer satisfaction.

- Bad Image: The low fleet size and aged fleet in turn has an impact on the brand.. currently in the routes where there is competition, Spicejet is the last choice, resulting in pressure on pricing.

- Weak Balance sheet: Despite a 4.5k crore fund raise, their balance sheet is not strong yet. Positive net worth was announced recently but the audited financials weren’t reflecting it. Also there was a qualification on current liabilities exceeding current assets by over 3500 cr. this may be due to non reflection of restructuring of lease liabilities but will have to wait for annual report to get clarity on this.

- Lack of enough cash for expansion: They have around 600 crore free cash as on 31st Mar’25 and around 400 cr to be received from an earlier fund raise.. so around 1000 crore which theoretically should be enough to take the fleet size to reasonable level, through un-grounding and new leases. However, unless they are able to generate good free cash flows with that fleet, adding newer planes might be difficult. Also any concerns over balance 400 cr receivable from the earlier fund raise will make things difficult.

- High free float/Selling pressure: Company has been issuing shares to multiple lessors as part of restructuring. While the deals are done at good valuations, selling keeps coming from such allottees as they don’t have investment interest in the company.

- Delay in un-grounding of planes: Co has earmarked around 650 cr for un-grounding of planes from the fund raise. The latest we know is that 450 cr was spent till March’25. However significant un-grounding hasn’t happened yet. This is a key monitorable.

- Pending litigations: There are few insolvency cases pending but the amount involved is not significant.

- Crude price (ATF price): Any significant increase in aviation fuel prices will have a significant impact on cash flows and margins.

- Boeing related concerns: Entire Spicejet’s fleet including future order placed, all are Boeing planes. Hence any negative development wrt to Boeing will have a significant impact on Spicejet operations. Negative US- India relations might also have an impact.

- Loosing rights over routes: Spicejet has rights over multiple domestic and international routes which it is not using due to lack of fleet and hence a chance of loosing those routes, while there is visible backing from current Govt.

Then why waste time and money for stock that was a clear no as per all fundamental lessons staring “The Intelligent Investor”? To understand that we will have to get into some details:

History (the drama that is no less than a Bollywood movie):

Ajay Singh bought a defunct airline in 2004, rebranded it to Spicejet, a Low Cost Carrier, started operations in 2005. The focus was to offer low prices, targeting tier 2 cities and higher efficiencies through aircraft utilization.

After initial success and good scale up, it was hit by global slowdown and surge in crude prices in 2008. Ajay, the BJP 2004 election campaign crafter, was suffocated due to pressures from lessors and ATF companies, airport infra entities – he was strangled from all sides.

In 2010, it was acquired by Kalanithi Maran, the then cabinet minister. While there is nothing in black and white but one can read between the lines on how the co was acquired.

Maran wanted the co to go aggressive, expanded to regional and international routes without bothering much on the bottom line..like any other startup in expansion mode. And by end 2014, Spicejet was in deep trouble with mounting losses, extremely weak balance sheet, low operational fleet, non-supportive lessors.

Through 2014 to 2015, history repeated for Spicejet, Ajay bought back the airline co for Rs. 2/- from Maran. While explicitly nothing is found but one can link the change in hands of Spicejet with change of power at centre. Revenge drama isn’t it?

Ajay turned around the company very swiftly, negotiated good deals with lessors, Govt. support helped, got good profitable routes, improved efficiencies and brought it into profits by 2017.

He also planned an aggressive expansion, everything was working great till early 2019, Spicejet became the second largest domestic carrier for a brief period.

However, grounding of Boeing Max hit it hard when 13 of its planes were grounded. That is a big hit on an aggressively expanding small airline company whose balance sheet just started recovering from shocks. While downfall of Jet airways helped Spicejet with slots and pilots, Covid hit very hard on Spicejet with mounting lease rentals, staff cost, parking and maintenance charges. While SpiceXpress, the cargo arm helped a bit, Spicejet was in deep trouble by 2023 with most of its aircrafts grounded.

In 2024 Ajay came-up with a restructuring plan wherein he committed to infuse 500 Cr capital and raise another 2500 Cr from investors. He faced difficulties in finding investors and closed the round at ~1050 Cr (of which received around 650 Cr). After getting some breakthrough in lease restructuring and other payments, Ajay was able to raise another 3000 cr from good set of investors.

As on date if what is told by the management is to be believed, majority of lease disputes are sorted, mainly with Carlyle aviation, grounded planes have started un-grounding, planning to double the fleet size from Mar’25 levels (25) by Dec’25, if everything goes right the fleet size might be 4x of Mar’25 levels by Mar’27, with ~100 aircrafts.

Current scenario of the company just managing to break even at operation level (or minor loss, if we discount some smart(?) accounting), is due the expenses incurred on non-revenue generating grounded fleet plus the lack of adequate fleet to take care of the fixed costs. The scenario could quickly change as more flights get ungrounded resulting in significant operational leverage.

So despite all the challenges, this is an interesting opportunity to evaluate at the current valuation.

Key updates since fund infusion by Ajay in September 2023:

Following is a summary of key events that happened in last ~24 months.

- Sept’2023 – Ajay Singh through Spice Healthcare invests ~500 Cr @ 30 per share through equity shares and warrants – 200 Cr comes upfront, ~300 Cr later. Along with this fund raise 231 Cr worth of lease receivables converted to equity @ 48 per share.

- 26th Jan’24 & Feb’24 – raises equity/warrants money of 1060 Cr @ 50 per share from multiple HNIs & Elara Capital, Areis Fund

- 16th Feb’24 – Ajay Singh along with Busy Bee Airways submits bid to acquire Gofirst, Spicejet to be the operating partner

- 1-7th Mar’24 – Settles disputes with aircraft lessors – AerCap (250 Cr) , Cross Ocean partners ( 93 Cr) & Eichelon Ireland (413 Cr) resulting in cost savings of 685 Cr, gets 3 airframes and engine

- 14th Mar’24 – Finalizes lease agreement for 10 aircrafts

- 26th Mar24 – Enters settlement with Export Development Canada, completed in Nov’24 ( 763 Cr settled for 190 Cr, gets 13 Q400 aircrafts), Nordiac Aviation (gets 6 aircrafts)

- 22nd May24 – Delhi HC bench rules in favour of Spicejet for a 450 cr refund from previous promoter Kalanithi Maran – He later filed appeal in SC against the order, SC dismissed the appeal.

- 7th Sept’24 – Restructures ~1150 Cr liabilities with Caryle Aviation for ~850 Cr, of which ~250 Cr as equity in Spicejet @ 100 per share, 170 Cr as CCDs in SpiceXpress.

- 20th Sept’24 – Raises 3000 Cr through QIP at 61.6 per share, from various FIIs and DIIs – strong names (Society Generali, Goldman Sachs, Morgan Stanley, Nomura, Discovery Global, Troo Capital, Citi, BoFA, BNP, Tata, Ashoka, Authum etc)

- Sept’24 – Carlyle Aviation has sold 2 Cr shares out of 5 Cr in the open market – price under check mostly due to this selling. Aeries also selling and has another 3 cr shares.

- 9th Oct’24 – Settles liability of 1100 cr with Babcock & Brown Aviation for 200 Cr, settles 200 cr liability with Aircastle for 40 Cr (completed in Nov’24)

- 16th Oct24 – DGCA removes Spicejet from enhanced surveillance (brought under surveillance from 24 Sep24)

- 30th Oct24 – Clears pending tax, PF, salary and other statutory dues worth 600 Cr

- 4th Nov24 – Acuite upgrades credit rating of Spicejet by 4 notches to B+.

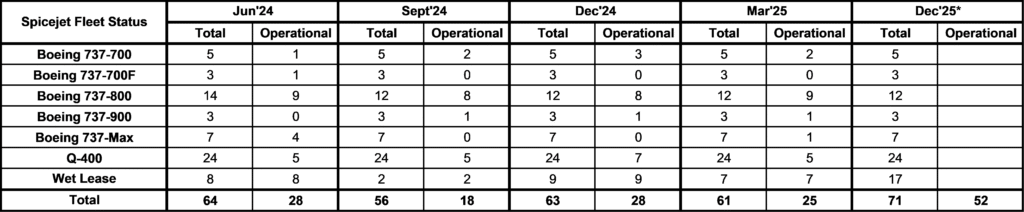

- Starts flights in various routes, got 10 additional planes on lease, 28 grounded flights to be ungrounded soon (only 28 of their existing 64 fleet count are operational currently).

- Dec’24 – Settles dues worth ~150 Cr with Genesis for 80 Cr, of which 50 Cr is cash payment, 30 Cr is through equity @ 100 per share.

- Jan’25 – Says that 10 planes would ungrounded by mid-Apr25, later re-inducts first 737 max plane.

- Jan’25 – Care assigns BB- rating, second rating upgrade in 3 months.

- Mar’25 – Ajay sells 3.15 cr shares to fund conversion of 13.15 Cr warrants (resulting in an infusion of 294 Cr).

- Mar’25 – settles dispute with Willis lease, insolvency petition withdrawn.

- Mar’25 – renews IATA IOSA (operational safety audit) certification till Mar’27.

- Apr’25 – launches daily nonstop flights to Khatmandu.

- May’25 – starts Haj operations by inducting two wide body aircrafts on lease.

- Jul’25 – SC dismisses Maran’s appeal for 1300 Crore.

- Aug’25 – No Level 1 safety issues found by DGCA in the last one year. Finalizes damp lease contracts to induct 10 Boeing 737 aircrafts.

Why am I invested?

Un-grounding Progress and Fleet Expansion:

The company had in Jan’25 projected un-grounding of 10 planes including 4 Boeing 737 max planes by mid April’25, of which 3 Boeing Max (and Max NG) were un-grounded. There were 17 engines sent for overhauling, two of which have come back. Considering the engine overhauling (which results in un-grounding) progress, reaching 52 fleet by Dec’25 doesn’t look far-fledged. In the last fortnight, they have in fact announced the induction of 10 Boeing 737 by Oct’25 on damp lease for the upcoming winter and early summary season.

(Note: With the 10 new aircrafts planned to be inducted in Oct’25, the fleet size becomes 38, up from 25 in Mar’25 and against the projected 52 in Dec’25)

Currently Spicejet is paying lease rentals, parking and other Airport charges plus maintenance for the grounded planes which are not generating any revenue. It managed to generate around 60 cr revenue per operational plane during recent quarter. Even if we keep Kumbh factor aside, ~45-50 cr revenue per plane per quarter with 8-10 cr EBITDA is possible if there are no costs for grounded planes. So with 50 fleet it has a potential to generate 2200-2500 Cr topline and 350-400 Cr EBITDA conservatively (just for reference, Indigo’s EBITDA margin is >30%). The progress towards this number would show us what rising like Phoenix means.

Potential SpiceXpress stake sale:

In May’23, there was an MoU announcement of $100 Mn investment by SRAM & MRAM in the subsidiary but no update post that. Also, there was a mention that Carlyle picked up stake (may be conversion of lease obligations) in SpiceXpress through CCDs worth 500 Cr at a future valuation of INR 12500 Cr!! (In another restructuring exercise in Sept’25, Carlyle had converted part lease liabilities into CCDs worth 170 Cr in SpiceXpress- valuation not disclosed). Any progress around this will be a huge plus, especially in the context of current of mcap of ~INR 4500 Cr for the entire company. Currently Spicejet holds 98% stake in the co (rest is esops).

Improving numbers:

While there is a significant delay in fleet expansion, the P&L looks much better in the half year ending Mar’25 when compared to Sept’24. Fund raising was completed in Sept’24 and settlements were happening till Mar’25 – so the positive impact of the efforts was only partially seen in the numbers, which are expected to improve going forward as well with the fleet enhancements, June’25 quarter might be subdued though.

The Ajay Singh factor & Govt. blessing:

Ajay Singh has been a turnaround specialist throughout his carrer, may it be Delhi transport corporation, loss making to profits in 3 years, Doordarshan restructuring with the launch of DD Sports and DD News, Spicejet launch in 2005, coming back to Spicejet in 2015 after selling it in 2010, turning it profitable within an year and keeping it profitable for next 18 quarters before the Boeing grounding, and even the recent attempt where he managed to raise >4k cr capital at a good valuation from well know global investors, he is credible.

In addition to this, Ajay Singh seems to be getting good backing – and may be part of the success is due to that. He was the one who played a critical role in BJP campaign in 2004 and 2014 and hence it is up to us to connect the dots. Getting back Spicejet at zero valuation in 2015, negotiating very sweet deals with lessors, Trump mentioning deal between Boeing and Spicejet (and hence the current strained relations between Modi-Trump could be a weakness), getting profitable routes, no negative impact despite high customer complaints, recent success in raising funds – it’s for the investor to understand and take a call. To me, the support will continue because if Spicejet were to be drowned, it would have happened in mid 2024. Not now.

Valuation comfort:

Fund raise valuation:

While Ajay infused capital at ~Rs. 30/- per share, first round of 1060 cr came at Rs. 50/- and next 3000 Cr came at Rs. 61.6/- So currently it is trading at ~50% discount to the recent fund-raise.

Restructuring:

Lease liabilities restructuring happened in various structures – a combination of haircut, cash payout and equity conversion. Wherever equity was issued, it was at a min of Rs. 65/- to as high as Rs. 100/-

SpiceXpress:

In 2023, Carlyle made an investment in SpiceXpress in the form of CCDs at a valuation of Rs. 12500 Cr. SpiceXpress currently contributes ~15% of the profits. Even after dilution, Spicejet would own >90% stake in this subsidiary, which gives a great valuation comfort.

Chart Check:

With the limited understanding I have, the chart suggest that the stock is trading in oversold territory.

Triggers to monitor closely:

- Un-grounding of planes and getting closer to 52 fleet mark targeted for Dec’25.

- Profitable Q1FY26 quarter which was quite challenging.

- Receiving balance ~400 Cr from earlier fund raise.

- AGM and annual report – market needs better clarity on the auditor qualifications.

- NSE listing – there was a plan but not executed yet.

- Stake sale in SpiceXpress or any such development.

- Win over Maran in its claim for 450 Crore. If not full, the interest part of 150 Crore.

Final Words:

For me, SpiceJet is a speculative turnaround bet with extremely high execution risks. But if the airline successfully un-grounds planes, expands its fleet, and stabilizes finances, the upside could be meaningful. This is not a stock for the faint-hearted — but precisely in such beaten-down counters that multi-baggers sometimes emerges.

Disclaimer:

I currently hold a position in Spicejet. These views are personal, not professional advice, and may carry bias. I am an individual investor and have had mixed experiences (including losses) in the past. Please evaluate independently before investing.